AML Screening & Transaction Monitoring Systems: Strengthen Compliance and Detect Financial Crime Faster

AML Screening and Transaction Monitoring Systems are crucial tools for financial institutions, using automated software with rules, AI, and machine learning to screen customer data against watchlists (like PEPs/sanctions) and continuously monitor transactions (deposits, transfers) for suspicious patterns (e.g., unusual volumes, high-risk jurisdictions) that signal money laundering or terrorist financing, flagging them for investigation and potential reporting as SARs to regulators, thereby ensuring compliance and protecting the firm.

AML Screening (Onboarding/Periodic)

- Purpose: Verifies customer identity and checks against known threats before or during a relationship begins.

- Process:

- Checks names against Sanctions Lists, Politically Exposed Persons (PEPs), and adverse media.

- Uses data from KYC (Know Your Customer) and CDD (Customer Due Diligence).

- Technology: Often uses database lookups, name matching algorithms.

AML Transaction Monitoring (Continuous)

- Purpose: Detects unusual or suspicious financial activity in real-time or near real-time.

- Process:

- Data Collection: Gathers transaction details (deposits, transfers, withdrawals).

- Rule-Based Analysis: Flags deviations from normal behavior (e.g., large cash deposits, rapid fund movement).

- Behavioral Analysis: Builds customer profiles to spot changes.

- AI/ML: Identifies complex patterns missed by basic rules, reducing false positives.

- Investigation: Compliance teams review alerts (true hits vs. false positives).

- Reporting: True hits lead to Suspicious Activity Reports (SARs) for law enforcement.

Key Technologies & Concepts

- Rules Engine: Predefined criteria for flagging activity.

- AI & Machine Learning: For advanced anomaly detection.

- Real-Time Monitoring: Immediate flagging of transactions.

- Risk-Based Approach: Tailoring monitoring to customer risk levels.

Why They Matter

- Regulatory Compliance: Fulfills legal obligations, avoiding fines.

- Reputation Protection: Prevents involvement in illicit finance.

- Financial Crime Prevention: Stops money laundering, terrorist financing, and fraud.

AML Screening & Transaction Monitoring Systems: Your AI Implementation Roadmap

Machine learning algorithms, particularly those optimized for streaming data, possess the computational power to analyze vast, complex datasets in real-time, identifying deviations from learned normal behavior with an accuracy unachievable by traditional methods.

Step 1: Architecting for Speed and Scalability in US Operations

Building real-time AI systems for AML and fraud detection in the U.S. necessitates meticulous architectural planning to accommodate immense transaction volumes, diverse data sources, and stringent data residency and compliance requirements.

- Implement High-Throughput Stream Processing: Leveraging technologies like Apache Kafka for ingesting and Apache Flink for processing high-volume, high-velocity transaction data streams is paramount. In deployments I've led, Kafka has proven indispensable for capturing every transaction event at source, ensuring zero data loss. For real-time processing and complex event analytics, Flink consistently delivers the required sub-second latency for critical decision-making in U.S. payment networks.

- Utilize Low-Latency Data Stores: Employing in-memory databases or highly optimized NoSQL stores ensures lightning-fast data retrieval during real-time analysis. Solutions such as Redis for caching frequently accessed customer profiles and Apache Cassandra for scalable, distributed historical data storage enable millisecond-level latency for critical lookups, a prerequisite for timely fraud intervention.

- Deploy Scalable Cloud Infrastructure: Leveraging leading cloud providers (AWS, Azure, Google Cloud) within U.S. regions is crucial for adherence to data residency and regulatory compliance. These platforms facilitate dynamic scaling of compute resources, critical for managing peak transaction loads, such as those observed during major U.S. retail events or market volatility. Auto-scaling groups are configured to precisely match compute resources to fluctuating demand, optimizing cost and performance.

- Strategic Edge AI Deployment (Use Cases Permitting): For initial, rapid fraud assessments, consider deploying lightweight AI models closer to the data source (e.g., at payment gateways or ATM networks). This can substantially reduce network latency and enable even faster initial assessments, providing an immediate, localized first line of defense, often reducing initial filtering time by orders of magnitude.

Step 2: Precision in Machine Learning Model Selection and Training

The choice of AI techniques directly correlates with the effectiveness and efficiency of your real-time monitoring system.

- Supervised Learning for Known Fraud Patterns (AI Fraud Detection): For established fraud typologies (e.g., credit card fraud, account takeovers, loan application fraud), supervised learning models are demonstrably effective. We typically train models such as Gradient Boosting Machines (XGBoost, LightGBM) or Random Forests on meticulously labeled historical data.

- Practical Feature Engineering for US Nuances: This stage is where deep domain expertise meets AI development. Focus on creating features that capture the unique behavioral nuances of U.S. financial transactions. This includes:

- Velocity Features: For example, "number of online purchase transactions to unique merchants exceeding $100 in the last 5 minutes."

- Geographic Anomaly: For example, "transaction initiated from a distinct IP address geolocated in a state more than 1,500 miles from the customer's usual transaction cluster within an hour."

- Value Deviations: For example, "transaction amount surpassing the 99th percentile of the 90-day moving average for this customer, or unusual patterns of micro-transactions consistent with 'smurfing'."

- Counterparty Analysis: For example, "number of transactions to entities identified on FinCEN's advisories or OFAC's SDN list."

- Continuous Model Training and Retraining: Financial crime patterns exhibit significant concept drift. Implement robust MLOps pipelines for continuous model retraining, incorporating fresh, validated data. Establishing a direct feedback loop where human analysts' confirmed fraud cases automatically enrich the training dataset ensures models remain highly relevant.

- Practical Feature Engineering for US Nuances: This stage is where deep domain expertise meets AI development. Focus on creating features that capture the unique behavioral nuances of U.S. financial transactions. This includes:

- Unsupervised Learning for Anomaly Detection AML (Zero-Day Threats): This capability forms your defense against novel or previously unseen financial crime schemes. Unsupervised learning algorithms identify transactions that statistically deviate significantly from learned "normal" behavior, without requiring prior labeling. This is critical for detecting "unknown unknowns."

- Isolation Forests: This algorithm efficiently identifies outliers in high-dimensional datasets. Its effectiveness stems from its ability to isolate anomalies with fewer splits than normal data points, making it exceptionally fast and scalable for real-time streaming data environments.

- Autoencoders (Deep Learning Fraud Detection): Implementing neural networks that learn a compressed, low-dimensional representation of normal transaction data is powerful. Transactions that cannot be accurately reconstructed by the autoencoder are statistically flagged as anomalous. I've found autoencoders particularly adept at detecting complex, multi-dimensional anomalies that might evade simpler rule-based systems, especially given the intricate patterns in U.S. consumer financial data.

- Graph Neural Networks (GNNs) for Network Analysis: Financial crime often manifests through intricate networks of individuals and entities. GNNs excel at analyzing relationships between accounts, customers, and transactions in real-time. They are invaluable for identifying suspicious clusters, uncovering complex money mule networks, or detecting obscured beneficial ownership structures, which are often employed in sophisticated U.S.-based money laundering schemes.

Intelligent Anomaly Detection: Moving Beyond Static Rules

The efficacy of real-time detection hinges on the sophistication of anomaly detection. This extends beyond merely flagging large transactions; it encompasses understanding context, discerning subtle behavioral patterns, and identifying statistical deviations from established "normal" behavior for a specific customer or entity.

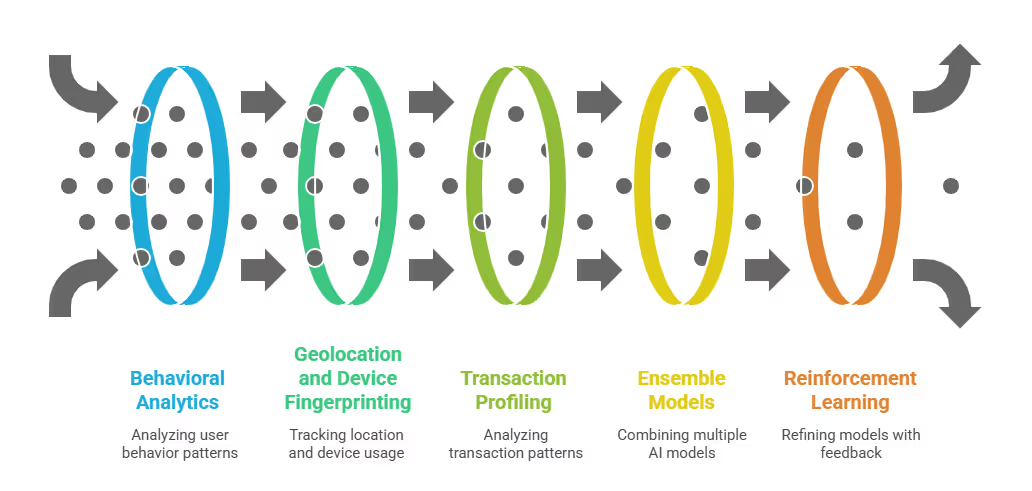

Behavioral Analytics Fraud Detection & Contextual Monitoring

To substantively reduce false positives and capture subtle illicit schemes, your AI system requires a deep understanding of user context.

- User Behavior Analytics (UBA): Construct AI models that create dynamic, evolving profiles of normal user behavior. This includes typical login times, transaction frequencies, device usage patterns, and usual geographic locations. Any statistically significant deviation from this baseline triggers an alert. For instance, a customer typically transacting from New York City who suddenly initiates a large-value wire transfer from an unrecognized IP address in a different U.S. state at an unusual hour would be flagged.

- Geolocation and Device Fingerprinting: Integrate real-time GPS or IP data with transaction locations to detect discrepancies (e.g., a transaction originating from an unusual IP address while the customer's usual mobile device is simultaneously active elsewhere). Device fingerprinting helps identify and track unique device identifiers to detect unusual access patterns or the suspicious use of multiple devices for a single account.

- Transaction Profiling (Predictive Analytics AML): Move beyond simple transaction amounts. AI analyzes the type of transaction, the counterparty, frequency, and historical patterns for that specific account. A sudden, statistically anomalous surge in small, frequent transactions to multiple unverified recipients might indicate layering in a money laundering scheme, even if individual transaction amounts are below traditional reporting thresholds.

Quantifiable Reduction of False Positives with Explainable AI AML

A significant pain point for U.S. compliance teams is the sheer volume of false positives. My objective as an AI architect is to engineer models that not only accurately detect illicit activity but also minimize the flagging of legitimate transactions.

This necessitates:

- Ensemble Models: Combining the predictions of multiple AI models (e.g., a supervised model for known fraud and an unsupervised model for anomalies) consistently improves overall accuracy and reduces false positives. A weighted voting system or stacking approach typically leads to more robust and reliable predictions.

- Reinforcement Learning for Continuous Improvement: This technique is powerful for adaptive learning. Implement a feedback mechanism where human analysts review alerts and explicitly label them as true positive or false positive. The AI model then uses this validated feedback to dynamically adjust its thresholds, refine feature importance, or even modify its internal parameters over time, continuously learning to better differentiate between legitimate and illicit activities.

- Explainable AI (XAI): Providing clear, interpretable reasons for why a particular transaction was flagged is not just a regulatory expectation (particularly from FinCEN and the OCC) but also operationally vital for compliance analysts. Implement techniques such as SHAP (SHapley Additive exPlanations) or LIME (Local Interpretable Model-agnostic Explanations) to offer transparency into model decisions. This critical transparency builds trust in the AI's judgment and empowers analysts to validate its findings efficiently.

Streamlining Suspicious Activity Reports (SARs) with Automated SAR

Once a suspicious activity is identified, the next critical step for any U.S. financial institution is generating a comprehensive Suspicious Activity Report (SAR) for FinCEN.

This process has historically been manual, resource-intensive, and susceptible to human error.

Your Path to Automated SAR Generation:

- Automated Data Aggregation: Design AI-driven systems to automatically pull relevant data points from disparate internal systems – transaction logs, customer due diligence (CDD) records, identity verification documents, communication logs, and external sources (e.g., OFAC sanctions lists, adverse media databases). This aggregated data is then systematically compiled into a structured format, ready for efficient reporting.

- Narrative Generation (NLP for Financial Crime): Leverage advanced Natural Language Processing (NLP) models to assist in generating initial narratives for SARs. These models can synthesize complex transaction data and contextual information into concise summaries of suspicious activity, linking related entities, transactions, and behaviors. While human oversight remains indispensable for final review and legal accuracy, this capability can reduce the manual effort in drafting narratives by up to 80%, a significant efficiency gain.

- AI Risk Scoring and Prioritization: Implement AI models to assign dynamic, data-driven risk scores to each case. This enables compliance teams to prioritize investigations based on the severity and potential impact of the suspicious activity. High-risk cases are automatically escalated for immediate human review, ensuring critical threats receive prompt attention.

- Regulatory Compliance AI US Checks: Train AI models on specific regulatory guidelines from FinCEN, the OCC, the Federal Reserve, and other relevant U.S. authorities. The AI can then automatically verify that all necessary information, as per reporting guidelines, is included in the SAR and that filing deadlines are met. This capability can measurably reduce the risk of non-compliance fines.

Overcoming Implementation Challenges in the US: A Data-Driven Playbook

Deploying AI in real-time AML and fraud detection in the U.S. presents distinct practical challenges.

Based on extensive hands-on experience, here’s a framework for navigating them:

Data Governance for AI in Finance: The Unwavering Foundation

- Data Quality and Unification: The U.S. financial sector often contends with heterogeneous data spread across legacy banking systems, diverse customer bases, and inconsistent data formats. This represents the single most significant barrier to AI adoption. Invest substantively in robust ETL (Extract, Transform, Load) pipelines to meticulously clean, normalize, and unify disparate data sources. Implement rigorous data governance policies to ensure data integrity, consistency, and lineage across the enterprise. This foundational data quality is directly correlated with AI model performance; models trained on poor data yield unreliable results.

- Data Labeling Strategy: For supervised learning models, accurate and consistent labeling of historical fraud and AML cases is paramount. This often requires intensive, collaborative efforts between data science teams and experienced compliance analysts to meticulously review past incidents and tag them correctly. Consider active learning strategies, where the AI model flags ambiguous cases for human review, thus intelligently improving its own training data quality and reducing manual labeling effort.

- Data Security and Privacy: Given the highly sensitive nature of U.S. customer financial data, unwavering adherence to U.S. data privacy laws (e.g., GLBA, CCPA where applicable) and stringent cybersecurity regulations is critical. Implement strong encryption protocols, granular access controls, and effective anonymization techniques. Explainable AI (XAI) also contributes to privacy by offering transparency without requiring raw, sensitive data exposure for every decision.

Building Your AI Implementation Roadmap AML Team & Capability

- In-house vs. Vendor Solutions: For product leaders, this is a pivotal decision. Building an in-house AI AML team demands significant investment in specialized data scientists, ML engineers, and deep domain experts. However, it offers unparalleled control and customization. Vendor solutions, conversely, can offer accelerated deployment timelines but may lack the granular customization required for unique U.S. market typologies. A hybrid approach, where a vendor provides a foundational platform and your in-house team customizes and enhances models, often strikes the optimal balance between speed and strategic control.

- Talent Acquisition and Upskilling (Building an In-house AI AML Team): The U.S. market for AI talent is highly competitive. Focus on attracting and retaining individuals with robust foundations in machine learning, distributed systems, and a genuine interest in financial crime deterrence. For existing compliance teams, invest in targeted upskilling programs to enhance their understanding of AI outputs, interpretation of XAI explanations, and ability to provide effective feedback for continuous model improvement. This bridges the critical gap between technical capabilities and domain expertise.

- Change Management: The deployment of AI fundamentally alters workflows for compliance teams. Anticipate and proactively manage resistance to change. Communicate the benefits transparently, provide comprehensive, hands-on training, and involve end-users in the development process to foster adoption and build trust in the new AI-driven processes.

Navigating the Regulatory Landscape (Regulatory Compliance AI US)

- FinCEN, OCC, Federal Reserve Guidelines: Continuous vigilance regarding the latest guidelines from FinCEN, the Office of the Comptroller of the Currency (OCC), the Federal Reserve, and other relevant U.S. regulatory bodies is non-negotiable. Your AI systems must be fully auditable and demonstrably compliant with these evolving regulations. Non-compliance carries significant financial penalties.

- Explainable AI for Auditors: U.S. regulators are increasingly scrutinizing AI models, demanding transparency. Be prepared to articulate precisely how your AI models arrive at their decisions. This is where your investment in XAI tools (SHAP, LIME) yields substantial dividends, providing the necessary transparency for both external auditors and internal governance committees.

- Regulatory Pilots and Innovation Offices: Actively engage with established regulatory innovation initiatives and sandboxes. These programs offer a controlled environment to test novel AI solutions, gather data on their efficacy and compliance, and potentially contribute to shaping future regulatory guidance for AI in financial services.

Quantifying ROI in AML: Proving Value to US Stakeholders

For product leaders, demonstrating a clear Return on Investment (ROI) is paramount for securing and sustaining AI investments in the U.S. financial market.

- Reduced False Positives: This is a direct, measurable metric. Track the percentage reduction in false alerts and the corresponding decrease in manual review time for your compliance analysts. Quantify the labor hours saved and the reallocation of these resources to higher-value investigative activities. Several leading U.S. financial institutions have reported false positive reductions of 70% or more with AI integration.

- Increased True Positive Rate (Fraud Prevention AI): Measure the quantifiable uplift in the detection rate of actual fraud and money laundering schemes that were historically missed by traditional systems. This directly translates into avoided financial losses and improved security. Some institutions have seen a 2x to 4x increase in genuinely suspicious activity identified after AI implementation.

- Faster Case Resolution: Track the average time taken from alert generation to SAR filing or case closure. AI-powered automation and improved alert accuracy should demonstrably shorten this cycle, impacting your operational efficiency positively.

- Operational Cost Savings: Quantify savings derived from reduced manual labor, minimized penalties for non-compliance, and overall improved operational efficiency. The global financial services industry spends an estimated $213 billion annually on compliance, with AI offering substantial avenues for cost optimization.

- Enhanced Regulatory Standing and Reputation: While challenging to quantify precisely, the ability to proactively detect and prevent financial crime bolsters your institution's reputation, cultivates deeper customer trust, and strengthens relationships with U.S. regulators. This can lead to reduced scrutiny and potentially fewer regulatory interventions.

The Future is Adaptive: Your Next Steps in Financial Crime Fighting

The financial crime landscape is a continuous evolutionary battle. We identified several key trajectories for AI in real-time AML and fraud detection in the U.S.:

- AI-Powered Cybersecurity Integration: The nexus between financial fraud and cybercrime is increasingly pronounced. Integrating AI-powered cybersecurity tools with your AML and fraud detection systems creates a holistic, multi-layered defense. This includes detecting phishing campaigns that lead to account takeovers or data breaches that precede larger financial crime schemes.

- Federated Learning Fraud Detection: For multi-bank collaborations or scenarios requiring data privacy across different institutions, federated learning holds significant promise. This advanced approach enables AI models to be trained on decentralized datasets without the raw data ever leaving the financial institution's premises, fostering collective intelligence while maintaining strict U.S. data privacy standards.

- Real-time AI Model Retraining: Beyond periodic retraining cycles, explore architectural designs that facilitate near real-time updates to models based on immediate feedback from validated fraud cases. This ensures your AI models are continuously adapting to the very latest criminal tactics, minimizing model decay.

- Synthetic Identity Fraud Detection Advancements: This rapidly growing threat in the U.S. demands sophisticated AI solutions. Focus on models that can cross-reference diverse data points from various sources (e.g., credit bureaus, public records, digital footprints) and identify subtle, statistical inconsistencies indicative of synthetic identities.

- Predictive Analytics AML for Proactive Interventions: Shift from merely detecting fraud to probabilistically predicting its likelihood. Leverage advanced predictive analytics AML models to assign dynamic risk scores at the customer level and even suggest proactive interventions, such as enhanced due diligence or specific product restrictions, before any suspicious activity materializes.

The transition to real-time, AI-powered AML and fraud detection is not merely a technological upgrade; it represents a strategic imperative for safeguarding the integrity of the U.S. financial system. By embracing advanced machine learning, prioritizing explainability, and fostering profound collaboration between your technology and compliance teams, your financial institution can transcend reactive measures and construct truly intelligent, adaptive defenses.

This journey involves navigating complexities related to data quality, legacy infrastructure integration, and nuanced regulatory interpretations. However, the quantifiable benefits – significant reductions in financial losses, enhanced compliance efficiency, and a more secure financial ecosystem – unequivocally justify this strategic investment.

Is your U.S. financial institution ready to elevate its financial crime defenses with cutting-edge AI?

Let's discuss how tailored real-time AML and fraud detection solutions can empower your compliance team and protect your assets.